Wall Street had a lot of expectations heading into 2023. Looking back 12 months later, it’s clear that most of them didn’t pan out.

To be sure, this is not that unusual. Wall Street strategists and economists have historically done a poor job anticipating what’s right around the corner.

But as those experts continue to debate why a recession that was once seen as virtually inevitable never materialized, or how inflation has managed to slow so dramatically without a meaningful rise in unemployment, a team of strategists at TSLombard has compiled a list of 10 of the most popular projections of 2023 that ultimately never came to pass.

As Wall Street strategists rush to revise their projections for 2024 to account for the powerful rally that has pushed the S&P 500 SPX to within 25 points of its record closing high from Jan. 3, 2022, the list offers a helpful reminder. The S&P 500 was trading at 4,756 on Wednesday, according to FactSet data.

See: It’s not even the new year, and Goldman Sachs has already lifted its S&P 500 target

But don’t take Wall Street’s projections for what might happen next year too seriously.

See: What 2024 S&P 500 forecasts really say about the stock market

All text and charts below are from TSLombard.

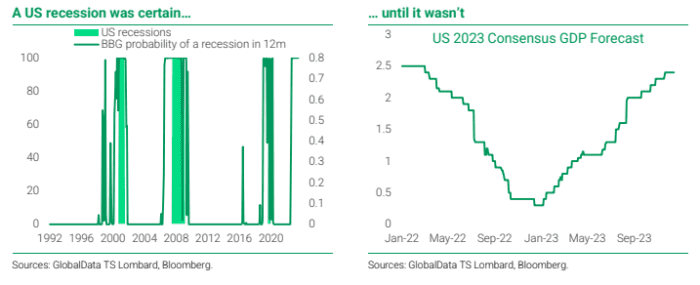

There was no U.S. recession.

“Heading into 2023 with an inverted yield curve, 425 [basis points] of Fed tightening behind us and real rates in restrictive territory, consensus shifted to a ~70% chance of recession (albeit a mild one). The Bloomberg US recession probability had jumped to 100% in August 2022 and remained there until the data stopped being published in June 2023.

TSLOMBARD

“However, the economy was more resilient to interest rate hikes than both we and consensus had expected. This was due to the long duration of US debt as well as to a large positive fiscal impulse and the associated high levels of net wealth. Not only did we not get a recession, but [third-quarter 2023 quarter-over-quarter] growth came in at 5.2%. Going into 2024, growth is expected to slow but a US soft landing is now the base case.”

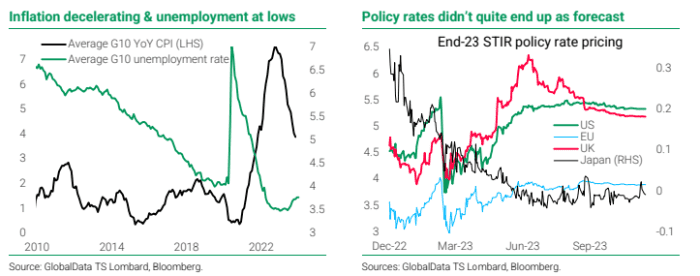

Unemployment didn’t need to rise for inflation to come down.

“The majority view was that in order to get inflation down amid demand pressures, there would need to be a sharp economic slowdown and a corresponding rise in unemployment. Amid the fake cycle, what we have had instead is supposedly immaculate disinflation; [monetary policy] tightening has reduced the number of job vacancies without putting people out of work, with demand destruction hitting the sectors where shortages were most pronounced. At the same time, the labour participation rate has risen.”

TSLOMBARD

The world’s biggest central banks didn’t cut rates.

“A recession meant that 2023 was going to be the year of the central bank pivot and cuts. While we did get some false starts — [short-term interest rate] markets were pricing in significant 2023 cuts when the [Silicon Valley Bank] crisis hit in March — in most cases, a resilient US economy allowed central banks to be more hawkish than originally expected by the market. Indeed, the [Federal Reserve] itself reached a terminal rate of 5.5% vs. the 2022 expectation of ~5%, while the [European Central Bank] has gone to 4% vs. the expectation of ~3%.”

The Bank of England never hiked rates to 6.5%.

“In the mini budget crisis, the STIR market rapidly re-evaluated the expected [Bank of England] terminal rate to 6.5; but with a new prime minister and a more sensible fiscal plan, that expectation settled back down to 4.7% at the beginning of 2023.

“However, we got a slightly less menacing re-evaluation into the summer, with the first leg up driven by UK growth upside surprises, followed by upside inflation surprises and a re-evaluation of term premia. But as the BoE had started tightening at the end of 2021 and most mortgages in the UK are for two to five years, it was only a matter of time for tightening to work its way through the economy.”

The Bank of Japan didn’t raise rates.

“At the end of 2022, markets were looking for the end of [negative-interest-rate policy] in Japan, with the policy rate priced to rise to 30 [basis points] in 2023. The market continuously tested the [Bank of Japan’s] dovish resolve, forcing the yen to a multi-decade low and persistently pushing [Japanese government bond] yields up against the yield cap.”

There was no banking crisis.

“We knew that after a decade of low rates and [quantitative easing], the transition to higher policy rates would be bumpy. One of those bumps was the [Silicon Valley Bank] collapse, which led to broader-based worries about the liquidity of regional banks and was followed shortly by the Credit Suisse buyout.

“At the time, we wrote that we didn’t expect a full-blown crisis, owing to the self-correcting nature of a rising interest rate-driven crisis, as well as the quick reaction of the authorities. Nor did we expect contagion across European banks. We were happily proved right.

“However, the crisis had even less impact than we had initially thought: credit conditions tightened but didn’t squeeze growth as much as we had anticipated.”

There was no U.S. government default.

“Amid increasingly polarized politics in the United States, markets got jittery in the second quarter, with US [credit default swap] spreads rising as the debt ceiling loomed once again. In June, we got the expected resolution but it was a reminder to investors of the structural issues with US govvies — something that markets were reminded of a couple months later when Fitch downgraded US debt to AA+ from AAA citing a growing debt burden and repeated debt-limit standoffs.”

China didn’t have a reopening boom.

“At the end of 2022, China exited Covid restrictions while at the same time stimulating and toning down ‘common prosperity’ messaging; it was meant to experience the reopening boom that had been seen in [developed markets] in 2021.

“However, as we pointed out at the time, stimulus was drip-feed, the property sector imposed a structural drag and related consumer behavior remained too cautious to spur growth. The economy is now stabilizing in what is an ‘L-shaped’ recovery, but the property contraction will continue for years and China’s new growth model is slower.”

The global property market didn’t collapse.

“Our colleague Dario Perkins identifies several reasons for this resilience: (i) expectations of imminent rate cuts; (ii) a sellers’ strike (the result of interest-rate ‘lock-ins’ and homeowner psychology); (iii) various ‘extend and pretend’ schemes, especially in the highest-risk markets (such as Canada); (iv) money illusion (reductions in real rather than nominal prices); (v) structural sources of demand (remote working and immigration); and (vi) the absence of ‘forced sellers’ thanks to continued strength in labor markets. It should be clear that while these forces have helped the soft-landing thesis in 2023, they do not rule out a hard landing in 2024. Thus, risks persist.”

Geopolitical shocks didn’t shock.

“Russia’s invasion of Ukraine in 2022 had a large impact on asset markets and economies but the adjustment was made in that same year. Supply chains were modified, infrastructure built and energy prices came down; markets moved on amid inherently un-discountable tail risks. In October, a conflict began between Israel-Hamas and the associated threat to oil supply saw energy prices spike. But once again, amid hard-to-price extreme geopolitical risk, markets simply moved on.”