“ This will not end well, but not yet. It’s still early in the bubble.”

Technical deteriorations in the U.S. stock market were apparent last week, but Nvidia Corp.’s NVDA, +4.00% blowout earnings report saved the day. The tech giant’s results beat Wall Street’s expectations on all metrics, and the company also guided upwards. There wasn’t anything to dislike about the report. As a consequence, the PHLX Semiconductor Index SOX, which is a bellwether for artificial-intelligence-related plays, rallied strongly.

Yet much like the dot-com bubble of the late 1990s, signs of excesses are evident. Still, I reiterate my view that the AI bubble has far more room to run before it reaches the phase of “magnificent exuberance.”

This is how a bubble builds. Consider General Electric Co. GE, +1.12%, which was one of the non-tech darlings of the late 1990s. Jack Welch, who was regarded as the superstar CEO of the day, demanded that division managers become either No. 1 or 2 in their business lines. If it failed to achieve those goals, the division was either shut down or sold.

Division managers who couldn’t make the numbers tried the old trick of financialization: GE would lend a customer money to buy its products and round-tripped the funds to inflate sales. The maneuver worked so well that GE Capital was born. GE Capital, in its efforts to achieve top-two status in its industry, lent to anything that moved. It wasn’t just aircraft engines, but emerging-market loans and subprime mortgages. GE Capital became bigger than the industrial divisions of the company and eventually blew up; GE CEO Jeff Immelt announced the divestment of GE Capital in 2014, and eventually its parts were sold off over the next two years.

“Today’s tech giants are buying equity in companies and round-tripping the funds to boost sales. ”

It’s happening again. Instead of vendor financing, today’s tech giants are buying equity in companies and round-tripping the funds to boost sales. Amazon.com Inc.’s AMZN, +0.83% investment in Anthropic and Nvidia’s investment in CoreWeave are just two of the most visible examples of financialization. As today’s market is focused on the prospect of total addressable market and sales growth, tech executives, who are mostly paid with stock-based compensation, are scrambling to boost sales growth at any cost.

This will not end well, but not yet. It’s still early in the bubble.

There have been some concerns raised about U.S. market-index concentration, as well. Those worries are mitigated by two factors. Concentration peaked in 1931–1932, instead of at the time of the October 1929 crash. Additionally, the current episode of increasing index concentration has been gentler and less sharp than the last two instances.

Valuations are also more reasonable than in the late-1990s dot-com bubble experience. The prices of technology and communication-services stocks are still closely tracking their earnings.

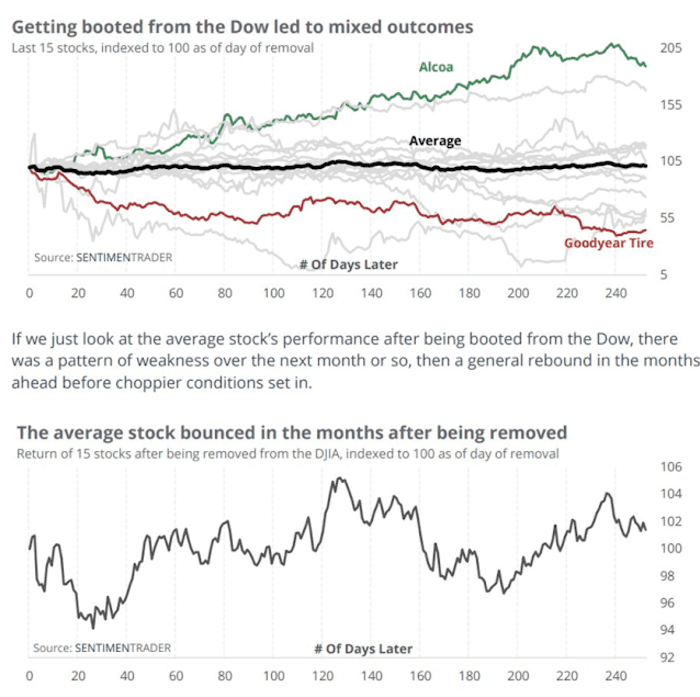

Yet there are a number of warnings of excesses to be worried about. Amazon is about to replace Walgreens Boots Alliance Inc. WBA, +1.08% in the Dow Jones Industrial Average DJIA. SentimenTrader has documented how being removed from the Dow has been, on average, a contrarian buy signal and how new additions have tended to lag the market.

The last time this happened was in 2020, when Salesforce Inc. CRM, +2.61% replaced Exxon Mobil Corp. XOM, +1.26%, which has been great for Exxon shareholders and not so much for Salesforce investors. So this latest change in the composition of the Dow may be a sign that Amazon, and growth stocks generally, are about to lag the market.

Read: Why Amazon and Uber investors might wish those stocks weren’t joining Dow indexes

More: After Nvidia’s latest blowout, here are 20 AI stocks expected to rise as much as 44%

AI’s virtuous cycle

“AI-driven productivity gains on top of current gains could spark a virtuous cycle of non-inflationary growth in the U.S. economy. ”

There is no question that AI will transform the way we work over the next decade and it will boost productivity. Even without the benefits of AI innovation, a study by Tuan Nguyen and Joseph Brusuelas at RSM showed a surge in U.S. total-factor productivity, which should encourage the Federal Reserve to overlook wage increases above inflation, as they will be offset by productivity gains.

During Nvidia’s earnings call, CEO Jensen Huang said that the company was seeing a “tipping point” in demand for AI systems. Moreover, he added, Nvidia’s latest results represent the first year of “a 10-year cycle of spreading this technology into every single industry.”

Putting it all together, AI-driven productivity gains on top of current gains could spark a virtuous cycle of non-inflationary growth in the U.S. economy. Such a scenario could lead to an AI-driven equity bubble of enormous proportions over the next few years.

What to watch out for

The market cycle currently is in the early phases of an AI-driven boom. Investor sentiment is inconsistent with the excesses seen at major market tops. As a reminder, here are some signs of excess of the dot-com era:

- Investors piled into Mannesmann, a German industrial conglomerate known mainly as a manufacturer of steel tubes, because it had a division that established Germany’s first cellular network. The company was eventually taken over by Vodafone for €190 billion, the largest takeover price paid at the time.

- Hutchison Whampoa, a holding conglomerate, became a TMT (tech/media/telecom) darling because of the telecom exposure of one division.

- Company presentations in disparate industries like mining and forestry always included a section titled “our broadband strategy.”

- The top was marked by a flood of low-quality IPOs. Remember all the B2B (business-to-business) and B2C (business-to-consumer) company offerings?

To be sure, some signs of froth are appearing, such as instances of financial engineering to boost sales. The Wall Street Journal also recently reported on how teenagers are jumping into the stock market using custodial accounts.

Custodial accounts for teens at Charles Schwab totaled close to 200,000 in 2022, up from about 120,000 in 2019, according to Schwab figures cited by the Journal. These further climbed above 300,000 in 2023, thanks in part to Schwab’s integration of TD Ameritrade. Other brokerages including Vanguard, Fidelity and Morgan Stanley’s E-Trade have also reported a surge in custodial accounts in recent years.

The latest BofA Global Fund Manager Survey showed that respondents had moved to a crowded long in technology stocks. While this may be a contrarian warning, it could be too early. History shows that such excessive overweight allocations can persist for years and for as long as the sector outperforms.

If I had to guess, the current AI-driven frenzy feels more like 1997–1998 than 1999 or 2000 of the dot-com era. The investment thesis is real and valid. Prices are just starting to surge. While the advance won’t be in a straight line, wait for the real signs of froth before turning cautious.

Cam Hui writes the investment blog Humble Student of the Markets, where this article first appeared. He is a former equity portfolio manager and sell-side analyst.

Also read: Ed Yardeni: Expect this ‘Roaring 2020s’ market to keep stocks up and bring inflation down

Plus: U.S.-China tensions over Taiwan threaten to derail Nvidia and other tech giants