Did a group of traders in rapidly expiring options recently drag the S&P 500 lower in the final hour of trading? Or has the influence of this booming corner of the options world been exaggerated?

A team of equity-derivative strategists at Bank of America BAC, -2.44% Global Research think it is the latter. In a research report shared with clients on Tuesday, the team argued that the impact of rising zero-day, or “0DTE,” volumes has been more benign than many on Wall Street believe.

0DTEs stand for zero days to expiration. They are option contracts typically linked to the S&P 500 or an S&P 500-tracking exchange-traded fund, like the SPDR S&P 500 Trust SPY, which have 24 hours or less until they expire.

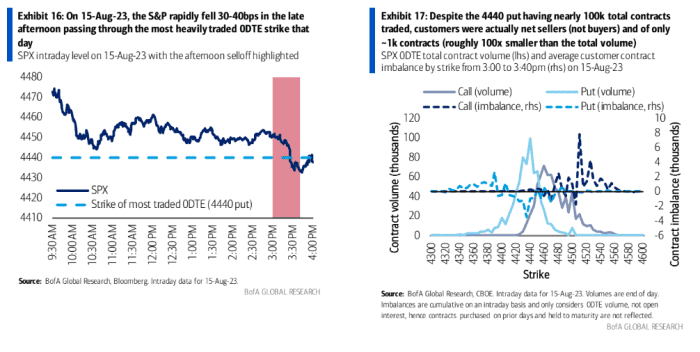

Analysts at Goldman Sachs Group GS, -1.02%, Nomura and other banks homed in on price action in stocks on Aug. 15, when the S&P 500 shed roughly 0.4% in a 20-minute period that also saw a flurry of trading in 0DTEs. The S&P 500 closed 1.2.% lower for the session, its biggest daily percentage drop in about two weeks, according to FactSet data.

Their thesis is that a wave of puts with a strike price around 4,440 moved into the money, forcing market-makers to hedge their positions by selling stocks and futures.

See: ‘This is no longer a buy-the-dip market.’ Why this Goldman Sachs veteran is worried about the stock market.

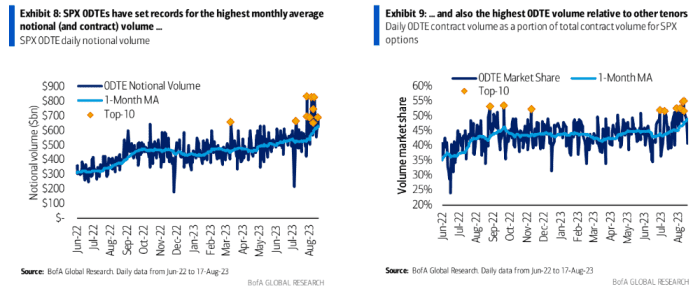

But a team of analysts at BofA has a different interpretation of what happened. To be sure, they acknowledged that 0DTE trading volume has grown dramatically in August to record highs. According to the team, eight of the 10 highest notional-volume days for S&P 500-linked 0DTEs occurred in the past 30 days.

The debate comes as investors endure a punishing month of August in stocks and bonds, sparked partly by a selloff in long-dated Treasurys that saw the 10-year yield BX:TMUBMUSD10Y touch its highest since 2007.

Through Friday, options on the verge of expiration were on track to see their busiest month ever in terms of notional volume traded. They also were on track to see records in terms of the number of contracts traded, as well as their share of total trading volume in S&P 500-linked options.

Zero-day options in their current form are fairly new. But trading in these options has boomed since last year when the CME Group and Cboe Global Markets, two major U.S. derivatives exchanges, introduced weekly options on certain indexes and ETFs with expirations every day of the trading week.

BANK OF AMERICA

Options give owners the right, but not the obligation, to buy or sell a given security at an agreed-upon price on or before an agreed-upon expiration date. Puts carry the option to sell, while calls carry the option to buy.

While the BofA team thinks 0DTEs have the potential to drive intraday instability in markets, a view that’s shared by many on Wall Street, they questioned the notion that zero-day option put buyers were responsible for what happened on Aug. 15.

Data cited by several Wall Street strategists showed roughly 100,000 0DTE put options with a strike at 4,440 changed hands after 3 p.m. Eastern. However, BofA’s analysis concluded that buy-side traders were net sellers of these contracts, not net buyers, as other analysts have concluded.

BANK OF AMERICA

Therefore, the team surmised that hedging by market makers, which other analysts have blamed for the sharp move lower in the S&P 500, didn’t have much of an impact, suggesting the late-day decline was likely driven by other factors like rising Treasury yields or trading by systematic quant funds.

“…[T]he impact 0DTEs may have had last week was clearly greatly overstated. Instead, other factors such as systematic quant flows…and the renewed impact of higher rates on equities may have been more relevant,” the team said.

See: Trading in risky ‘0DTE’ stock options hits record and could spark a stock-market selloff, strategists say

To be sure, analyzing option-market flow data isn’t an exact science, leaving some room for interpretation as analysts try to discern whether a given trade involved a buy-side trader buying calls or puts from a market maker, or something else, according to Brent Kochuba, founder of SpotGamma, a provider of data and analytics for the derivatives market.

U.S. stocks have fallen since the start of August, with the S&P 500 SPX down 4.4% through Tuesday’s close, according to FactSet data. The Nasdaq Composite COMP has fallen by 5.9%, while the Dow Jones Industrial Average DJIA is down 3.6%.