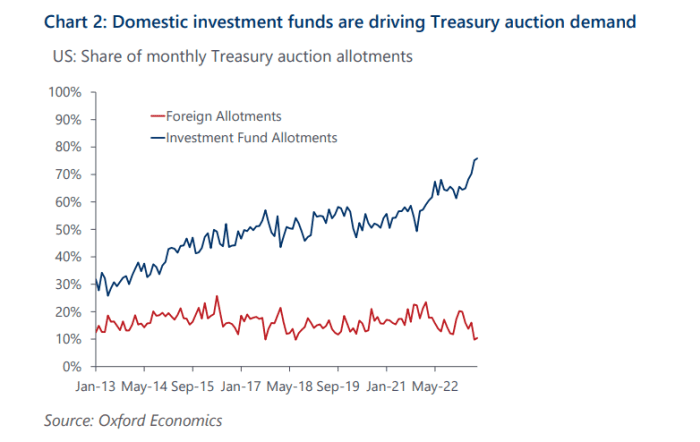

The recent deluge of Treasurys sold at auction has gone mostly to domestic investment funds, according to Oxford Economics.

Domestic funds snapped up about 76% of July’s Treasury auction supply, marking the fourth straight month in a row of a record share, according to an Oxford tally, while foreign allotments have been weaker.

Domestic funds are snapping up most Treasury auctions

Oxford Economics

“Investment funds have been the primary, and growing, source of demand for Treasury coupon auctions, particularly since auction sizes began to decline in late 2021,” said John Canavan, lead analyst at Oxford Economics.

“But the main question mark for the market’s ability to absorb the increased Treasury coupon issuance will be whether or not the increasing demand from domestic investment funds continues.”

Treasury bill issuance is expected to total $ 728 billion in the third quarter, and $ 402 billion in the fourth-quarter, according to a forecast by BofA Global’s rates team on Friday. That’s largely to help refill the Treasury cash account run low by the long debt-ceiling battle.

The tally would put issuance for the second half of 2023 at $ 1.13 trillion, a huge amount but also a bit below the Treasury’s $ 1.3 trillion forecast, according to BofA Global.

Appetite for safe, high-yields

“I think it will be digested relatively well,” said BMO Wealth Management’s Yung-Yu Ma, chief investment officer, in a phone interview, adding that U.S. rates versus other developed countries remain high.

“I think there is quite large appetite for safe, high-yield debt, and short-term Treasury securities certainly offer a nice yield.”

Yields on short-term Treasury securities that mature in less than a year have been relatively steady in the past week, with the 1-month bill rate BX:TMUBMUSD01M at 5.34% on Friday, according to FactSet.

Bigger moves have been seen this week in the 10-year Treasury yield, BX:TMUBMUSD10Y which briefly traded above 4.2%, marching higher in the wake of Fitch stripping the U.S. of its top AAA rating, and a $ 1 trillion funding estimate from the Treasury for the third quarter.

“The 10-year above 4% is telling us there’s some stickiness to the upside for rates,” BMO’s Ma said. “I think rangebound is good,” he said, adding that a 3.8% to 4.2% range for the 10-year yield probably works well for equities, but a big drop in the benchmark yield could signal greater economic weakness.

Stocks were higher Friday, but with the S&P 500 index SPX, Dow Jones Industrial Average DJIA and Nasdaq Composite Index COMP remained on pace for weekly declines, according to FactSet.

Bigger picture, a recession isn’t something Ma thinks is likely. “We were talking about a soft landing when it was very unpopular,” he said. “The elements of a soft landing should still be in place because the labor market is providing a buffer from Fed interest rates.”

Read: U.S. adds 187,000 jobs in July and points to hiring slowdown. Wages still high