From disease and downturn to the deterioration in Chinese-American relations, there has been no let-up to the blows battering the world’s trading system. The latest threat stems from the possibility of another global recession. Only two years after the world sank into a covid-induced slump, shipping bosses are again warning of grim prospects for international trade.

But beyond the ups and downs of the economic cycle, deeper shifts in global trade patterns are taking place. Firms are reconsidering their production decisions, and governments are pushing the process along. Such shifts might have seemed outlandish in 2018 when Donald Trump, then America’s president, first slapped tariffs on imported Chinese goods. Since then, Joe Biden’s administration has banned the export of advanced semiconductor technology to China and plans to provide subsidies worth hundreds of billions of dollars for investment in domestic manufacturing. A rejigging of trade flows now feels inevitable rather than unimaginable—and the outline of the new geography of international trade is becoming clearer.

Global trade in goods staged an impressive bounceback after the covid-induced downturn of 2020. As a share of world gdp, the value of such trade last year rose to its highest since 2014. But not all trade routes are flourishing. When Mr Trump took his protectionist turn, there was hope that economies in Africa and Latin America might attract some of the business that would have otherwise flowed to China. That has not happened. Instead, the biggest winners from changing trade patterns are to be found in Asia.

Global trade data emerge slowly, meaning figures on imports to big economies are the best way to get an up-to-date picture of what is happening. According to American data released on November 3rd, the country’s imports have risen by a third since 2018. Gains, though, have been uneven. American imports of Chinese goods stand just 6% above the level of four years ago, a hefty decline in China’s market share since Mr Trump launched his trade war. America’s imports from eu have also grown in lacklustre fashion, up by just 12% since 2018. “Friendshoring” may be happening, but not on a grand scale. Imports from Canada and Mexico have risen by 39% and 34% respectively.

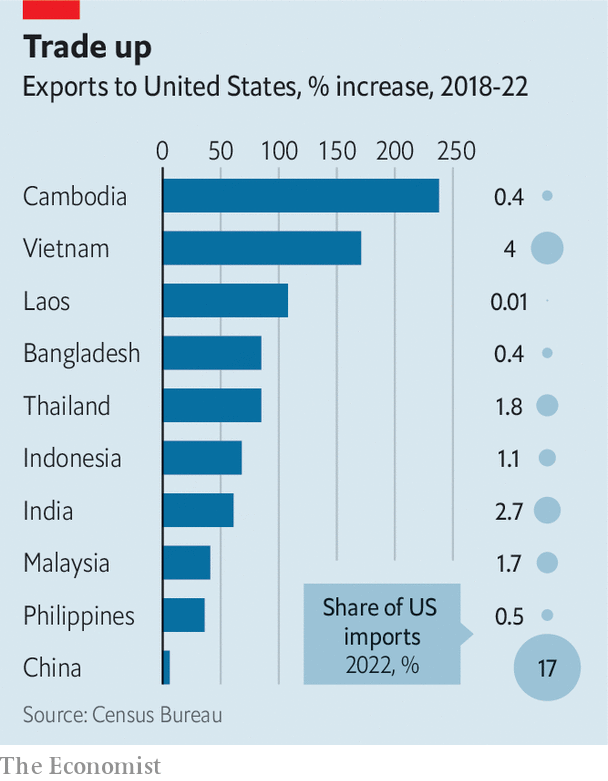

The great champions of the past four years are instead in Asia. Exports to America from Bangladesh and Thailand have jumped by more than 80% since 2018; exports from Vietnam are up by more than 170% (see chart). India and Indonesia have seen their exports grow by more than 60%. All of this means that China’s share of American imports dropped by four percentage points between 2018 and 2022, from 21% to 17%. China used to account for nearly half of Asia’s exports to America; now it accounts for just over a third.

Nor is this simply an American trend. China is also importing more from Asia. Over the first nine months of this year, the share of China’s imports coming from America fell by two percentage points compared with the same period in 2018. The share coming from the eu declined by a similar amount. On the other hand, the Association of South-East Asian Nations (asean), a group of ten countries, saw its share of China’s imports grow by two percentage points. European trade figures are less up-to-date, but Asia’s rise is also visible in them. Although the share of eu imports from China rose last year, so did those from South and South-East Asia. Neither China or Europe saw a comparable rise in imports from other regions of the world.

Cultivating new sources of goods or components takes time and investment, so the shift in trade patterns now visible in the data mostly reflects choices firms made well before this year’s geopolitical ructions. Some redistribution of trade would have happened even in placid economic conditions. Rising labour costs in China, for instance, would have made it attractive to move low-value sorts of manufacturing—in textiles and apparel, say—to places like Bangladesh.

Yet Mr Trump’s tariffs seem to have played an important role. According to recent analysis of industry data by Chad Bown of the Peterson Institute for International Economics, a think-tank, China’s share of America’s imports rose from 36% to 39% this year in goods not covered by tariffs. For goods subject to a 7.5% tariff, however, China’s share sank from 24% to 18%. And for those hit by a whopping 25% tariff, which covers lots of it equipment, China’s share of imports fell from 16% to 10%. Overall America is now much less dependent on Chinese goods, from furniture to semiconductors.

This change may not be quite as radical as it appears at first glance. It seems likely that many of the components used to make goods in India or Vietnam are themselves produced in China. Although the detailed supply-chain data needed to say for sure will not be published for several years, Chinese export figures are certainly suggestive. The two-percentage-point drop in the share of China’s total exports destined for America over the period from 2018 to 2022 is exactly matched by the increase in China’s exports to asean economies.

The story so far seems to be one in which Asia’s emerging economies increasingly intermediate trade between China and the rich world. Dreams that supply chains draped across Latin America and Africa would remake the world’s economic geography are still just dreams. But this direction of travel is an unalloyed boon for a rapidly growing arc of countries stretching from India to the Philippines. In time, as the consequences of recent geopolitical developments accumulate, an ever larger share of the value in Asian supply chains may concentrate outside of China rather than within it. ?