Harsha Upadhyaya the Chief Investment Officer, Equity at Kotak Mutual Fund

Harsha Upadhyaya, Chief Investment Officer, Equity, Kotak Mutual Fund, spoke about the resilience of Indian markets and how they will be affected by changes in global markets in the coming months.

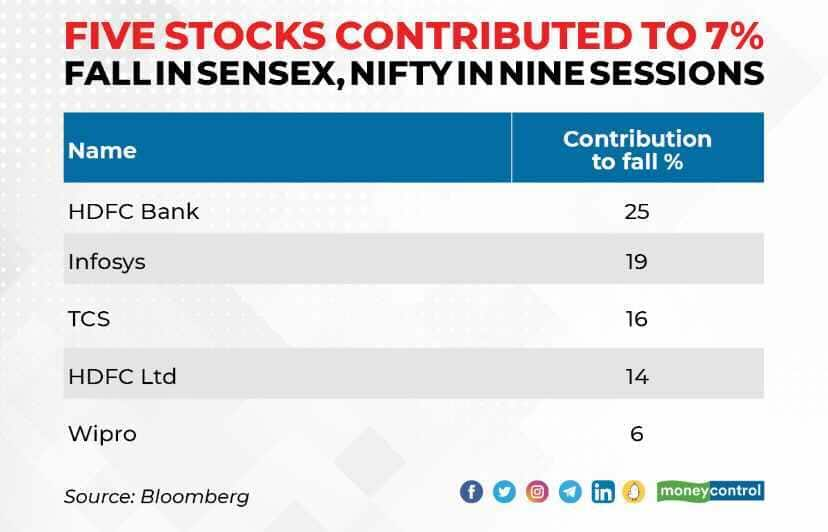

Speaking about his stock and sector picks, Upadhyaya told CNBC TV18 in an interview: “We continue to remain underweight in the IT sector. In the very short term, global cues may lend some stability to the IT sector, however we believe that 2023 IT budgets would be softer than we expect.”

Below are edited excerpts from the interview:

It’s like Diwali in the market. Do you think the index has legs to run across 18,000, and more, given the global tailwinds?

I think Indian markets have been very resilient compared to what’s happening in global markets. Of late, we have also seen some of the global cues improving a bit, though there is going to be more volatility in the next few months, I guess. Nevertheless, I think stability in global markets has aided Indian markets, where earnings have been more or less per expectations this quarter, which in turn lends stability to the markets.

The last time we chatted you were positive on the auto segment. Maruti’s numbers look good. The auto rally has played out quite a bit, but do you believe it still has legs?

When you look at the auto segment overall, there is some more steam left. Most auto segments are seeing strong volume growth as commodity prices are easing. In passenger vehicles, we are seeing chip supplies improve a bit, as well as a lot of new product launches, which has generated a lot of positive consumer interest. The volume growth we have seen in the recent past should continue with the same momentum over the next few quarters, and margins should also improve as we go ahead. We believe the valuations do not factor in all this upside as yet.

After some drubbing, Nykaa is in the green . Where do you stand on e-commerce stocks? Many of them have a lock-in, but would you pick some of the good businesses in the dips ?

Valuations have been expensive for most of these e-commerce businesses compared to traditional ones. Everyone agrees that what’s getting factored in the markets now is the fact that the lock-ins are going to end soon, leading to more supply, and that’s creating an overhang. Most of these stocks where the end of the lock-in is imminent are seeing that kind of pressure.

We feel that if you are confident of the business then you should have a bottom-up approach, looking at a firm’s fundamentals. Every e-commerce stock is not the same in terms of business or valuation.

The global economy is challenging. But do you think we are perhaps better off than we were about six-eight months ago? In that context, how do you view IT stocks that have underperformed? Also, how do you view Dr Reddy’s, which has been the top performer on the Nifty today

We continue to remain underweight on the IT sector, but yes, in the very-short term global cues may lend some stability to the sector. However, we believe that 2023 IT budgets would be softer than we expect. Even when you look at the management commentary of IT firms in the recent past, it indicates that there are pockets of weakness among their various customer segments, such as retail, mortgage, high-tech, etc. Our belief is we will see more weakness as we go into 2023.

While margins have held up until now, with weakening demand you could also see pressure on margins. We believe that rather than IT, some other domestic-facing sectors will have much more headroom for growth if markets continue to do well.

Similarly, in pharma, we continue to be stock-specific. We are not looking at a top-down stance in this segment. We remain quite underweight in both these segments.

You have been positive on the banking sector. If credit continues to grow, the worst of asset quality issues may be behind us, at least in the near-term. Do you think PSU banks deserve a second look, because if you look at the past one year, they’ve done decently even though they may not have made much money ?

We do have some exposure to PSU banks, and they’ve done well. One of the concerns about this segment was how treasury yields would move, and how that would impact their income.

But treasury yields have been broadly within a range and I don’t think that’s going to negatively impact some of the PSU banks, at least in the immediate-term.

As far as the cost of funding is concerned, they are in a very good position in terms of CASA (current and savings accounts) levels, and we believe that that is critical. If you have a low cost of funding when interest rates are moving up, that’s going to aid margins. Asset quality issues are behind us and credit is growing month-on-month.

We remain positive on the overall banking space, and within that we are positive on large private sector banks which have very good CASA on their books, and also on large public sector banks.

Everybody has a buy on the State Bank of India (SBI) and Bank of Baroda (BoB). Will you be looking at smaller banks as well?

No, we would remain in the larger banks because that’s where we have stability in terms of CASA.

Your thoughts on urban consumption? How do you view the Quick Service Restaurant (QSR) space, or names like Trent and Aditya Birla Fashion & Retail (ABFRL)?

Urban consumption continues to be quite strong as we have seen during the festive season. We expect that to continue. But rural is still somewhat weak. However, each of these pockets are very different in terms of business drivers, so we’ll have to evaluate each of them differently.

For the first time in more than a decade, the NHPC (National Hydroelectric Power Corporation) climbed very fast and crossed its issue price. Likewise, Tata Power has also performed decently, though it’s been more volatile. Any thoughts on power stocks ?

It’s not been a very big focus area for us, but we do have a small exposure on a couple of names in our portfolio. We don’t see much of a re-rating from these levels for some of these power utilities, but yes, they will provide stability to the overall portfolio.

We’ve been throwing sectors at you. You tell us what your preferences are?

As I mentioned, we are positive on banking and auto. We are also overweight on the industrial sector, where the investment cycle has been picking up after a long time. Some of these stocks are very healthy, with good order books and balance sheets. So we should see a decent re-rating in the medium- to long-term.

We are also positive on manufacturing segments such as cement, chemicals, etc., where we continue to see growth, and believe that margins should also start improving as commodity cost pressures decline.