Netflix Inc. has become a value stock — a bargain, according to Charles Lemonides, chief investment officer at ValueWorks in New York.

During a year that has featured a re-rating for so many rapidly growing companies that had been trading at lofty valuations to earnings, Netflix Inc. NFLX, +2.63% has fallen enough to make its stock compelling, Lemonides said in an interview.

“The extended part of the market is extended no more,” he said, calling Netflix an even better buy at $ 173.10 a share (where it closed on May 9) than when he bought the stock at $ 225 “on the way down” in April.

The stock hit its intraday high of $ 700.99 on Nov. 19.

The idea of buying shares of Netflix following a decline of 71% so far this year (and 75% from its high) may seem radical, but Lemonides, whose team manages about $ 250 million for private clients, makes a strong argument.

“It seems really easy for them to manage 10% revenue growth and have margins improve,” he said.

Many investors and traders describe themselves as “contrarians.” If you are really a contrarian investor who aims to take advantage of low prices when making long-term investments, such a dramatic pullback warrants a closer look.

The Netflix value case

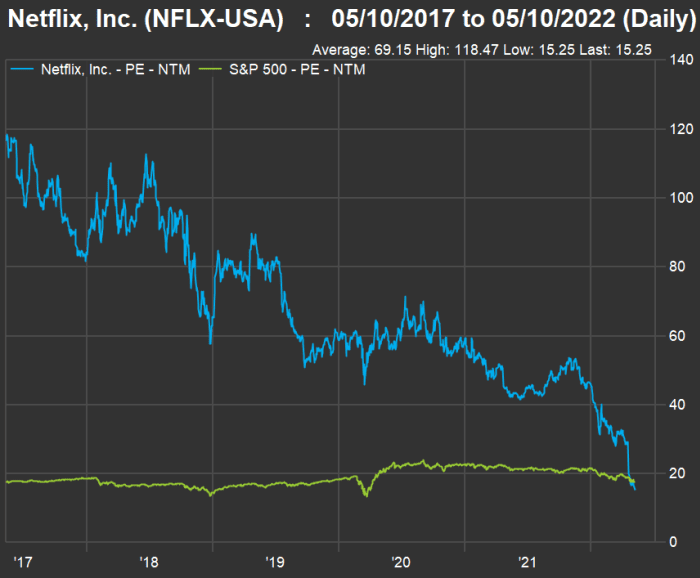

This chart shows the movement of forward price-to-earnings ratios, based on consensus earnings estimates for rolling 12-month periods, over the past five years for Netflix and the benchmark S&P 500 Index SPX, +0.25% :

FactSet

At the close on May 9, Netflix traded for 15.3 times the consensus earnings-per-share estimate among analysts polled by FactSet. The S&P 500 traded at a weighted forward price-to-earnings ratio of 17.6. Looking back, you can see that over the past five years, Netflix has traded at much higher valuations to expected earnings, with an average forward P/E of 69.2.

What has turned investors against Netflix is the perception that its best years of growth are behind it. When reporting its results on April 19, Netflix said its paid user base had declined by 200,000 accounts during the first quarter and estimated it would lose 2 million paid subscribers during the second quarter. This shocked investors and pushed the stock down 35% in one trading session on April 20. To put that 2 million number in perspective, Netflix said it had about 220 million “paying households.”

But what about revenue, earnings and profit margins?

- Netflix’s first-quarter revenue totaled $ 7.87 billion, up 2% from the fourth quarter (despite the decline in paid accounts) and up 10% from the first quarter of 2021.

- Earnings per share for the first quarter were $ 3.53, compared with $ 1.33 the previous quarter (when spending on content was much higher) and $ 3.75 a year earlier.

- Netflix’s operating margin (essentially, earnings before interest, taxes, depreciation and amortization, divided by sales) during the “terrible” first quarter was 66.25%, according to FactSet. This measure of profitability isn’t available for most companies in the financial and real estate sectors. But among the 445 companies in the S&P 500 for which FactSet calculates quarterly operating margins, Netflix ranked 16th (or in the top 4%). For the S&P 500 (which, again, trades at a higher P/E than Netflix), FactSet estimates the weighted first-quarter operating margin was 15.93%. Over the past five quarters, Netflix’s operating margin has ranged from 57.55% to 66.25%.

- The company’s net income margin (net income divided by revenue) for the first quarter was 20.30%, which ranks at 133 among the S&P 500 per the most recent quarterly numbers available. By this measure, Netflix ranks within the top third.

Netflix is a solidly profitable company, even though its entire business model has been based on subscription fees, with no advertising revenue.

Lemonides said Netflix will have an easy time growing revenue and earnings in part because of the potential to convert some shared accounts to paying accounts. In its first-quarter earnings press release, the company said that in addition to the 220 million households paying monthly subscription fees, an estimated 100 million more households were using the service for free through account sharing.

Netflix plays nice

Netflix executives outlined a patient, respectful approach to monetize account sharing.

During the company’s earnings call on April 19, Netflix Chairman and co-founder Reed Hastings said Netflix was “working on how to monetize sharing,” which hadn’t been a priority when its paid user base was growing rapidly. The big advantage is that these estimated 100 million households already “love the service,” he said.

Netflix chief operating and product officer Gregory Peters said the sharing viewers presented a “tremendous opportunity” because “they have everything they need to get to Netflix.” He pointed to what may be a customer-friendly way of capturing additional revenue by “asking our members to pay a bit more to share the

service with folks outside their home.”

Peter continued: “So if you’ve got a sister, let’s say, that’s living in a different city — you want to share Netflix with her, that’s great. We’re not trying to shut down that sharing, but we’re going to ask you to pay a bit more to be able to share with her, so that she gets the benefit and the value of the service, but we also get the revenue associated with that viewing.”

The ‘paid net additions’ problem

The focus on “paid net additions” to its number of user accounts served Netflix well when it was adding viewers very quickly, but a focus away from revenue and profit may not serve a maturing company well.

When asked if Netflix and other companies that previously focused on growth of user numbers instead of sales and earnings might not be able to change investors’ perceptions, Lemonides said: “There are valuations at which [user] growth is needed to have any semblance of support.”

But now, with the stock trading at 15 times expected earnings and his expectations for earnings to grow, “you have shifted to not needing user metrics,” he said.

When asked about the time frame for an investment in Netflix, Lemonides said he is willing to hold the stock for seven years.

“Some time between now and seven years from now, this company will become a mature, major cash generator,” he said.