Venkat Viswanathan, Founder, LatentView

“We are a GOPGC,” LatentView Analytics Founder and Chairman Venkat Viswanathan says at the beginning of our interview.

Intrigued, we ask him what is GOPGC? “Good, old-fashioned, profitable growth company,” he explains.

Being old-fashioned and profitable is probably what the Indian markets need at this point, after Paytm’s initial public offering (IPO) debacle, which has cast a shadow over the plans of other heavily funded and unprofitable internet companies that had lined up listing plans in the coming months.

LatentView Analytics, by those metrics, is an atypical company, almost a breath of fresh air. It is completely bootstrapped, extremely low-profile and has been profitable from day 1.

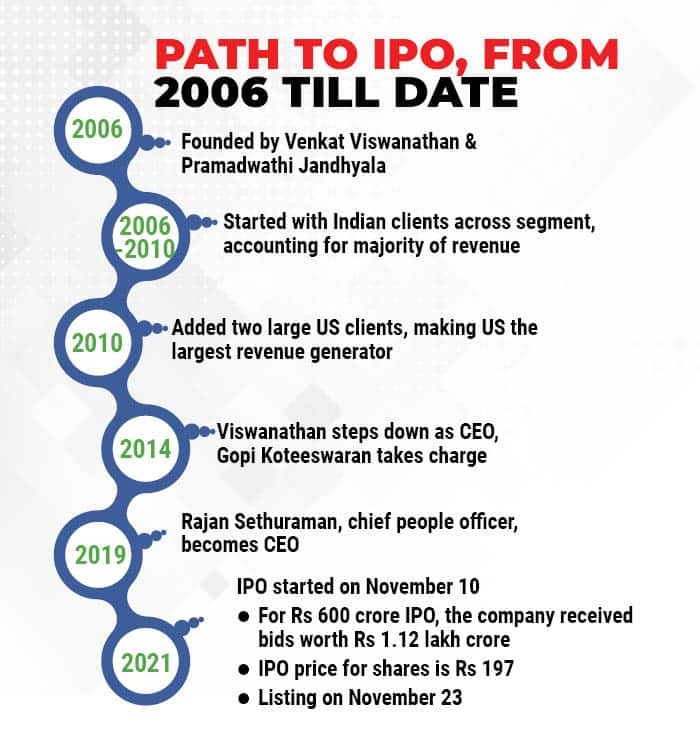

Founded in 2006, LatentView offers data analytics services, consulting, and data engineering solutions to customers across the banking, technology, industrial, and retail verticals, among others. In its 15 years of existence, the company has reported a loss only for one quarter, in early 2010. Viswanathan, an alumnus of IIT Madras and IIM Kolkata, worked at Cognizant before he started up.

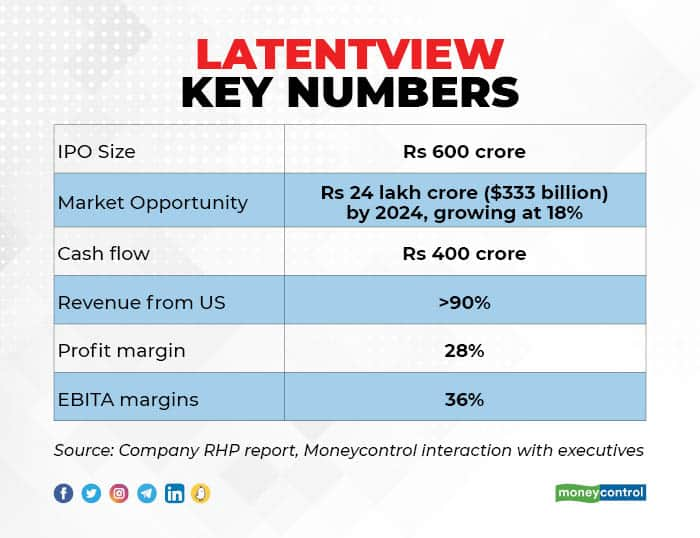

The Chennai-based firm was in the spotlight recently when its IPO registered a record subscription. Its issue was oversubscribed 338 times, much higher than the high-profile internet IPOs that were listed over the last couple of weeks: Nykaa, Paytm and PolicyBazaar.

LatentView listed on the Indian stock exchanges on November 23, 2021 and had a bumper opening with stocks trading at Rs 512.20, from IPO price that was fixed between Rs 190-197.

In this interview with Moneycontrol, founder Viswanathan and CEO Rajan Sethuraman talk about going public, the overwhelming investor interest, being profitable, and building a bootstrapped company for 15 years.

Rajan Sethuraman, CEO, LatentView

Rajan Sethuraman, CEO, LatentView

Edited excerpts:

Let me start with the humongous response for the IPO. You were planning to raise Rs 600 crore, but you got bids worth Rs 1.12 lakh crore. What did you make of the huge interest from investors?

Sethuraman: Clearly, the response was much bigger than what we imagined it to be, or what we were expecting it to be. There has been a slew of internet IPOs, and given the nature of the businesses they are in, they may not be profitable at this point in time.

So I think, within that spectrum, we are, in some sense, a breath of fresh air in actually demonstrating a very profitable trajectory through the years and it is also a very high-margin profitable business even within the data and analytics spectrum. Our revenue per employee is $ 65,000.

So, in our case, it’s a combination of not only the profitable track record that we have demonstrated but also the potential that the future holds for us. But this is beyond our wildest imaginations. I think it just shows that the Indian market is also mature, it’s coming of age and there are a lot of young investors who understand what technology is all about, and what such businesses can be in the years to come.

What made you go for the IPO now?

Viswanathan: I think if you look at our journey, we are a bootstrapped business. We have never raised equity capital ever before. The promoters own almost 80 percent of the company, before the IPO. Post IPO dilution, it will probably be about 68 percent. People keep asking me the question, ‘why such a small issue when you could have raised so much more. And our view is that the 68 percent is a lot more valuable for us. I keep joking about how it feels like I’m giving away a kidney and so I want to give as small a portion of the kidney as I can, live comfortably, and see it grow.

As for why now, I think in any company’s journey, it’s very important to kind of seize the moment and convert the opportunity that you see into good prospects for the business. I believe data analytics has come mainstream only in the last five years, even though we’ve been around 15 years. I still remember when we used to meet customers in 2006-2008. We had to first explain to them what data analytics is. But that’s not the case anymore. Today, we have inbound conversations with some of the best companies in the world. In fact, if you look at our clients, two-thirds of our customers are technology companies in Silicon Valley.

These are all digital native pioneers, who are inventing all this technology and they still need help. And they are choosing us as their partner. We are also very conscious that we just a Rs 300 crore company, a small company even in India, forget the global scale. But we are in the right market and we can actually make a much bigger impact in the market if we raise adequate capital.

Sethuraman: There’s a saying right, don’t waste a crisis. In some sense, the pandemic has presented an opportunity as well. So in some sense, we do see an inflection point in the last 2-3 quarters, and there has been a significant shift in terms of the number of conversations and the kind of opportunities that our clients are interested in going after as well.

Launching a data analytics company in 2006 would not have been easy since, as you said, you had to convince clients. So, could you take me through your journey from 2006 till now? You have built the company largely staying under the radar.

Viswanathan: Just before we started LatentView, I spent about seven years in Cognizant. I joined the company a few months after they had just gone public on NASDAQ. At that time, we were still less than 1,500 people. I keep joking — where everyone was on the same floor and Lakshmi (Narayanan, then President of Cognizant) had to walk past me every day if he wanted to go to the restroom. So, I was in a strategic seat, so we knew we could kind of catch up whenever I wanted, as a smaller company.

By the time I left, they were already more than a billion dollars in revenue. I had a very small role to play as a cog in the wheel. But it was a fantastic training ground and I learned a lot. When I started, 2006-2008 were not easy years. We were first-generation entrepreneurs and had humble beginnings. I keep joking that in Chennai, we don’t have the equivalent of the garage startup since we barely had space for people to live.

It took us about a couple of years trying to even figure out what our market is, what is our offering. In the early days, we kept ourselves servicing clients in India, like in Mumbai and Delhi. Multinationals and financial services were early clients. Then we started getting some traction in the US, which we realised was a much bigger market and much more valuable. We also made a conscious choice that we will sell only to the really largest companies in the world, the rich customers, as we like to call them. We decided that we wouldn’t focus on SMEs, and we won’t sell to companies that are not profitable.

If there was ever a quarter in our 15-year journey where we probably did not make money, or we actually went into the red, that was probably the January-March quarter of 2010. But as I keep telling people, good things happen to good people, and we just had to stay the course. Soon in July that year, we won two large American clients. Overnight, we went from having 80 percent revenue from India to 90-95 percent of revenue from the US, which is where we stayed pretty much from 2010 to 2021.

You’ve only posted a loss once?

Viswanathan: If memory serves me right it would be from January to March 2010, just at the tail end of the global financial crisis. Even during the crisis, we were doing okay, but towards the end, one of our Indian customers decided to pull the plug on us and gave us an ultimatum.

But nothing changed. For every six weeks that I spent in India, I would spend two weeks in the US. In any year, it was seven to eight trips to the US. So constantly, you’re on a plane. And when we land in the US, it is like, how many cities can we cram into the nine days. I typically fly out on a Thursday evening from New York, so that you can arrive Saturday early morning in India, and then the family is okay, you are here for the weekend.

We have this principle and I still believe in it, which is, it takes six meetings before you can win a customer on average. There is no resistance to persistence. So, don’t give up after a couple of meetings, you have to keep turning up, keep turning up. The first two deals that we got in 2010 changed our fortunes and it happened when I was sitting in the US for two weeks.

Could you have grown even faster and scaled up? What are some calls that you took on growing and scaling at a certain pace?

Viswanathan: We never raised external capital and we are completely bootstrapped. Most of the things we do are like traditional companies. This is how businesses have been built over the last 100 years, where it’s not about just throwing money at it. So, our customers are really our biggest investors in us.

We don’t cut corners there. But if you ask our people, are we paying the most? And are we doing all kinds of lavish expenses? They’ll probably be the first to say no, we are frugal. Again, I keep joking. We are a ‘thayir sadam’ (curd rice) company and just like to keep it very simple.

But, would you have grown faster if you had raised any funding?

Viswanathan: It is a very conscious choice to pick a pace of growth that we believe is long-term sustainable, and which does not need valuation like other companies that have raised a lot of money. It is not as if they will leapfrog to a scale and we are nowhere in comparison. We are all in a similar ballpark, maybe a few 100 crores this way that way and it’s a matter of time before we all kind of become a tight-knit, small set of companies running around. Like, one of the professors told us early on, it is good if you learn to live on lean milk and no fat, so that if you’re given high-fat milk, you know how to process it. If you do the reverse, it doesn’t work.

If I look at your financials, your profit is Rs 90 crore on revenue of Rs 300 crore. So, your profit margins are actually comparable to large IT services companies, I think it’s in the ballpark of 25 percent. Should we benchmark you against them in terms of growth rate, margin, margins, and so on now that you are entering the listed universe?

Sethuraman: I think we have averaged between 25-28 percent in terms of EBITDA margins, and that’s the range that we feel comfortable with at this point in time. Last year, there was a bit of a spike and went up all the way to 34 percent. But that’s on the back of several things that have happened – pandemic-related reduction in travel and marketing expenses. There is also increased acceptance of more work being done offshore, which might go back as companies start opening up their offices. Even within the spectrum of work that we were doing, we decided to exit a part of the business, which was providing point expertise, and focused only on the Manage services type of work. So, in some sense, the margin has improved on account of that. I’m expecting that we will comfortably hold that 20-25 percent rate in the coming quarters.

In the last two to three years, we have had a bit of a flattish profile on account of a few reasons. There was the active reshaping of the business that I talked about. There were at least 8-10 accounts that we decided to exit because we didn’t see them as enduring relationships. There were one or two accounts that were impacted either by the pandemic and decided to completely stop work or alternatively do things in-house. So, a combination of all of that has meant a bit of a flattish profile. The last two three quarters though have come back strong and we are back at a 20 percent-plus growth rate year-on-year and 7-11 percent quarter-on-quarter.

A lot of this is down to choices we make, and we are much more comfortable being conservative and running it in a way where we do not having to worry about our future. If you look at our balance sheet, you will find that we had Rs 400 crore of cash even before we went public.

With that kind of cash flow, why do you need to tap public markets?

Viswanathan: Visibility. You saw what happened in the market. Our talent acquisition team has been working very hard in a market like the current year where everybody is switching jobs. You can see what this may have as a payoff. “Have you heard of LatentView?” Hopefully, we don’t have to answer that. That is on the talent supply chain. But even on the customer side, I think it is a great validation for a lot of customers

Did you get any offers to be bought in the last decade or so? There was a time when IT companies were talking about analytics firms.

Viswanathan: You are asking this to a person who didn’t want to give 0.1 percent of their kidney, to sell their whole body. So, people have asked us. We even considered a particular deal with a European company at some point.

Of course, you can never say never for the right reasons, and for the right price, everybody is up for sale. We are not denying that. I will be the first to accept we are not visionaries. It is not as if we knew in 2006 that analytics will be the biggest thing in 2021 and everybody will be talking about AI and ML. We didn’t know that. But now that we have stumbled upon it, we have some great achievements, and a great team, who have been co-owners of this business. If we have all this, why don’t we do justice to the opportunity? If at all we have to sell it, why don’t we do it when we are a multi-billion-dollar firm and why get out this early? So, for the right reasons, it is possible. But just for money, we are not interested in all those things.