2023 has been a great year for stocks and a number of other markets, but the number of winners narrows if you run the tape back to the beginning of last year, just before the Federal Reserve and other major central banks delivered a massive rate shock, noted analysts at Deutsche Bank in a Friday note.

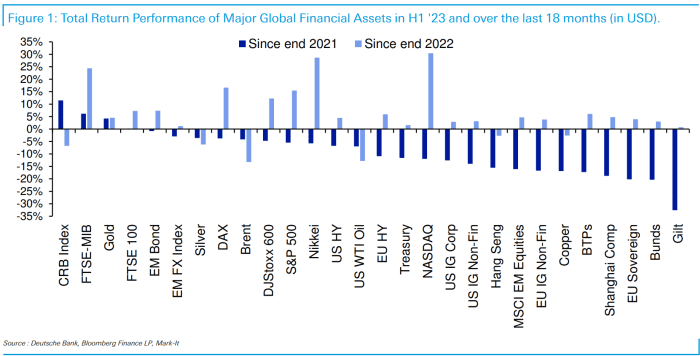

With investors and traders set to close the books Friday on the second quarter and first half of 2023, the chart below runs down the performance of major financial assets in 2023 and over the last 18 months. Performance since 2022, in U.S. dollar terms, is represented by the purple bars, with first-half performance represented by the light blue bars:

Deutsche Bank

The era of higher rates started in early 2022, when the yield on the 10-year Treasury note TMUBMUSD10Y, 3.825% jumped from 1.5% to 2.5% by the first week of April and then jumped to just below 3.5% by the middle of June last year, macro strategist Jim Reid noted. The 10-year now trades around 3.86%.

Back at the start of 2022 the yield on the 10-year German bund TMBMKDE-10Y, 2.394% was still at -0.18%, then rose to 1.77% by mid-June 2022 and now stands at 2.44%.

The rate shock has set the tone over the last 18 months. While U.S. long-term rates have stabilized at higher levels over the last 6 to 12 months, the chart shows that the damage to assets perceived as risky remains “very evident” from the early part of the period, Reid said.

“At the start of this year we felt H1 (the first half) would be OK for risk assets but that problems would build as the recession approached later in H2. H1 has surprised on the upside, largely due to tech and AI, but if the start of 2022 marked the start of a new higher rates era, then these returns should still be seen in that context,” he wrote.

That said, the more positive interpretation “would be that we had a one-off rate shock that the market sharply adjusted to and that we are now in the process of normalizing and can continue to leave the shock behind us as we progress through the quarters ahead,” Reid said.

The Nasdaq-100 NDX, +1.51% was on track for its best first-half performance since records began in 1986, while the Nasdaq Composite COMP, +1.38%, up nearly 30% year to date, was on track for its best first half in four decades. The S&P 500 SPX, +1.08% was up 14.5% so far in 2023, while the Dow Jones Industrial Average DJIA, +0.71% lagged behind, up 2.5%.

Don’t miss: These are the best-performing stocks in the 2023 bull market — and the worst

Reid noted that going back to the beginning of 2022, the winners are very narrow, as the chart shows, with commodities, gold GC00, +0.47% and Italian equities I945, +1.08% isolated at the top.

Adjusted for inflation of around 8%, only commodities have slightly outperformed, he noted, while British government bonds, or gilts, have dropped around 33% in dollar terms and over 40% in real terms. That’s the sort of wipeout that “could take a decade to make back in nominal terms and much longer in real terms,” Reid said.