While the IRS says most employees can only contribute $ 22,500 to tax-deferred income to 401(k) plans in 2023, top executives at U.S. companies can defer much more than that if they participate in special nonqualified deferred compensation programs known as “top hat” plans.

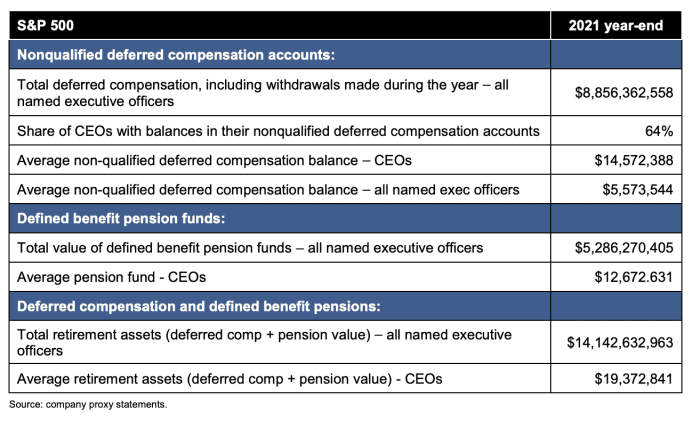

Some of the details of those plans are available in dense corporate filings, with specifics on the top officers in the company. In 2021, the top executives at S&P 500 SPX, +1.19% firms held a combined $ 8.9 billion in these nonqualified tax-deferred (NQDC) accounts, according to a new study from the Institute for Policy Studies and Jobs for Justice called “A Tale of Two Retirements,” that added up the line items reported.

For instance, the latest proxy statement for Walmart WMT, -0.17% filed with the SEC shows the balances of deferred compensation of seven top executives, including Chief Executive Doug McMillon, who had an aggregate balance of $ 169 million in his deferred compensation account at the end of 2022. That balance currently earns a “fixed rate of interest set annually based on the 10-year Treasury note TMUBMUSD10Y, 3.562% yield on the first business day of January plus 2.70%,” according to the filing, but Walmart is moving toward a more open system for contributions made beginning in fiscal year 2024 that will be market-based, the statement notes.

While the SEC filings show just the most highly paid executives, more than 700,000 employees are able to participate in these kinds of plans at over 11,000 companies, according to a survey by MBS Financial Group, an administrator of nonqualified executive benefits. The average plan holds $ 16 million and the average participant balance is $ 265,000.

The “Tale of Two Retirements” study looks at major corporations and their top executives, including companies like Hyatt Hotels H, +0.44%, Home Depot HD, +3.56%, Centene CNC, +2.67% and Pfizer PFE, -0.70%. It found that 64% of CEOs at these types of companies participated in top-hat plans, and of those that did, the average balance was $ 14.6 million.

Credit: Institute for Policy Studies and Jobs for Justice report, “A Tale of Two Retirements.”

“Executives owe income taxes on this compensation when they withdraw the funds, but in the meantime, they benefit from the tax-free compounding of investment returns,” says Sarah Anderson, director of the Global Economy Project at the Institute for Policy Studies.

Tipping the hat for executives

So-called “top hat” plans are allowed by the IRS as a form of executive compensation. The plans are subject to retirement plan regulations (Erisa), but not part of the annual 401(k) contribution limits. Executives can actually participate in both, deferring up to the 401(k) limit annually and contributing to the nonqualified options. These NQDC plans can take many forms. Some only hold contributions in company stock and some hold it in fixed income, while others allow the employees to choose their investments. Some companies put limits on how much can be contributed, while others allow unlimited amounts.

The benefit to the employee is tax deferral, while the benefit to the company is retention. The money set aside grows tax-free until the employee withdraws it, either at retirement or when they leave the company. The potential massive tax hit can help convince some executives to stay put in their jobs.

One major potential detriment is that these holdings are not protected from creditors, as 401(k) funds would be. “If the company goes bankrupt, you’re out of luck,” says Steven Golden, managing director at CSG Partners, an investment bank based in New York. “Most people don’t think of the worst-case scenario, but honestly, it would cause me anxiety. In some cases, it’s a lot of money.”

Golden also points out that top-hat plans merely delay taxes, they don’t erase the obligation. “You’re better off getting the money up front and investing it after tax, just to protect that part,” he says.

More from Beth Pinsker

That 401(k) match isn’t just free money, 3% could buy you two years of retirement

How to get starting investing with an investing club

Forget that $ 22,500 limit. Some workers can supersize their tax-deferred retirement savings up to $ 265,000 in 2023.