Let’s get ready to rumble.

The Federal Reserve and investors appear to be locked in what one veteran market watcher has described as an epic game of “chicken.” What Fed Chair Jerome Powell says Wednesday could determine the winner.

Here’s the conflict. Fed policy makers have steadily insisted that the fed-funds rate, now at 4.25% to 4.5%, must rise above 5% and, importantly, stay there as the central bank attempts to bring inflation back to its 2% target. Fed-funds futures, however, show money-market traders aren’t fully convinced the rate will top 5%. Perhaps more galling to Fed officials, traders expect the central bank to deliver cuts by year-end.

Stock-market investors have also bought into the latter policy “pivot” scenario, fueling a January surge for beaten down technology and growth stocks, which are particularly interest rate-sensitive. Treasury bonds have rallied, pulling down yields across the curve. And the U.S. dollar has weakened.

Cruisin’ for a bruisin’?

To some market watchers, investors now appear way too big for their breeches. They expect Powell to attempt to take them down a peg or two.

How so? Look for Powell to be “unambiguously hawkish,” when he holds a news conference following the conclusion of the Fed’s two-day policy meeting on Wednesday, said Jose Torres, senior economist at Interactive Brokers, in a phone interview.

“Hawkish” is market lingo used to describe a central banker sounding tough on inflation and less worried about economic growth.

In Powell’s case, that would likely mean emphasizing that the labor market remains significantly out of balance, calling for a significant reduction in job openings that will require monetary policy to remain restrictive for a long period, Torres said.

If Powell sounds sufficiently hawkish, “financial conditions will tighten up quickly,” Torres said, in a phone interview. Treasury yields “would rise, tech would drop and the dollar would rise after a message like that.” If not, then expect the tech and Treasury rally to continue and the dollar to get softer.

Hanging loose

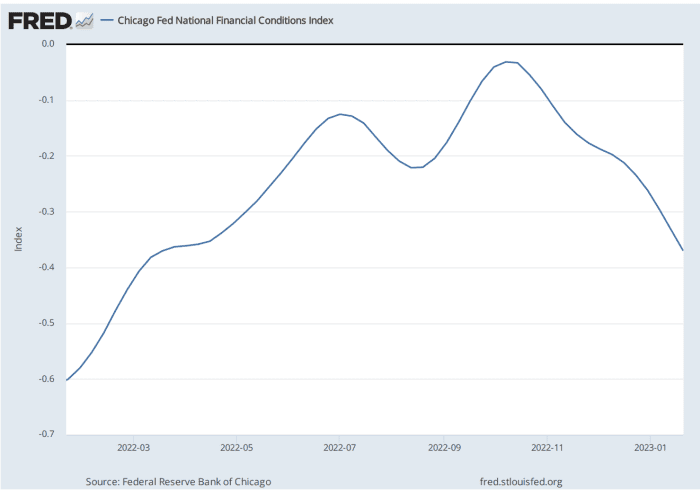

Indeed, it’s a loosening of financial conditions that’s seen trying Powell’s patience. Looser conditions are represented by a tightening of credit spreads, lower borrowing costs, and higher stock prices that contribute to speculative activity and increased risk taking, which helps fuel inflation. It also helps weaken the dollar, contributes to inflation through higher import costs, Torres said, noting that indexes measuring financial conditions have fallen for 14 straight weeks.

The Chicago Fed’s National Financial Conditions Index provides a weekly update on U.S. financial conditions. Positive values have been historically associated with tighter-than-average financial conditions, while negative values have been historically associated with looser-than-average financial conditions.

Federal Reserve Bank of Chicago, fred.stlouisfed.org

Powell and the Fed have certainly expressed concerns about the potential for loose financial conditions to undercut their inflation-fighting efforts.

The minutes of the Fed’s December meeting. released in early January, contained this attention-grabbing line: “Participants noted that, because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability.”

That was taken by some investors as a sign that the Fed wasn’t eager to see a sustained stock market rally and might even be inclined to punish financial markets if conditions loosened too far.

Read: The Fed delivered a message to the stock market: Big rallies will prolong pain

If that interpretation is correct, it underlines the notion that the Fed “put” — the central bank’s seemingly longstanding willingness to respond to a plunging market with a loosening of policy — is largely kaput.

Major indexes were mostly lower in choppy trade to kick off the week, with the Dow Jones Industrial Average DJIA, -0.07% shaking off an early dip to rise 44 points, or 0.1%, while the S&P 500 SPX, -0.59% shed 0.5% and the Nasdaq Composite dropped 1.3%.

Investors will be sifting through the busiest week of earnings season, which will include results from Amazon.com Inc. AMZN, -1.83%, Apple Inc. AAPL, -1.25% and Facebook parent Meta Platforms Inc. META, -2.06%. Stocks rallied last week, with the S&P 500 and Nasdaq Composite logging their highest closes of the new year. The Nasdaq was on track for its best January since 2021.

See: Tech stocks are having their best January in decades — here’s why that may not be a good sign

Meanwhile, the Fed is almost universally expected to deliver a 25 basis point rate increase on Wednesday. That is a downshift from the series of outsize 75 and 50 basis point hikes it delivered over the course of 2022.

Data showing U.S. inflation continues to slow after peaking at a roughly four-decade high last summer alongside expectations for a much weaker, and potentially recessionary, economy in 2023 have stoked bets the Fed won’t be as aggressive as advertised. But a pickup in gasoline and food prices could make for a bounce in January inflation readings, he said, which would give Powell another cudgel to beat back market expectations for easier policy in future meetings.

Jackson Hole redux

Torres sees the setup heading into this week’s Fed meeting as similar to the run-up to Powell’s speech at an annual central banking symposium in Jackson Hole, Wyoming, last August, in which he delivered a blunt message that the fight against inflation meant economic pain ahead. That spelled doom for what proved to be another of 2022’s many bear-market rallies, starting a slide that took stocks to their lows for the year in October.

But some question how frustrated policy makers really are with the current backdrop.

Sure, financial conditions have loosened in recent weeks, but they remain far tighter than they were a year ago before the Fed embarked on its aggressive tightening campaign, said Kelsey Berro, portfolio manager at J.P. Morgan Asset Management, in a phone interview.

“So from a holistic perspective, the Fed feels they are getting policy more restrictive,” she said, as evidenced, for example, by the significant rise in mortgage rates over the past year.

Still, it’s likely the Fed’s message this week will continue to emphasize that the recent slowing in inflation isn’t enough to declare victory and that further hikes are in the pipeline, Berro said.

Too soon for a shift

For investors and traders, the focus will be on whether Powell continues to emphasize that the biggest risk is the Fed doing too little on the inflation front or shifts to a message that acknowledges the possibility the Fed could overdo it and sink the economy, Berro said.

She expects Powell to eventually deliver that message, but this week’s news conference is probably too early. The Fed won’t update the so-called dot plot, a compilation of forecasts by individual policy makers, or its staff economic forecasts until its March meeting.

That could prove to be a disappointment for investors hoping for a decisive showdown this week.

“Unfortunately, this is the kind of meeting that could end up being anticlimactic,” Berro said.