The Federal Reserve isn’t as mysterious as it’s made out to be. It’s not hiding coded messages in its communications. It’s not using obscure metaphors that seem to say one thing but actually mean the opposite. There’s no secret chord that only the truly devout can hear.

When Fed policy makers said, as they did in the summary minutes of their July 26-27 meeting, that they are all “highly attentive to inflation risks,” they meant it. When they said that “there was little evidence to date that inflation pressures were subsiding,” they meant it. When they said that inflation “would likely stay uncomfortably high for some time,” they meant it.

Read more coverage: Federal Reserve officials back moving interest rates higher to slow the economy, minutes show

Resolutely hawkish

And above all, they meant it when they unanimously agreed that the risk of persistently high inflation made it necessary to raise the federal funds FF00, -0.00% target range by 0.75 percentage points to 2.25% to 2.50% last month, and that they anticipated that “ongoing increases in the target range would be appropriate.”

The Fed remains resolutely hawkish (biased toward higher interest rates). There was no hidden, secret dovish message in the July 26-27 minutes. But some people found one any way.

As MarketWatch’s Isabel Wang reported Thursday, many participants in the stock market misread the minutes initially on Wednesday, thinking that the Fed was secretly getting cold feet and was hinting at a “dovish pivot.” But by Thursday’s trading session, the market seemed to have a handle on what the Fed was actually communicating.

“ Just talking about a risk doesn’t mean the Fed will act on it. ”

One of the confusing things about the Fed is that it has adopted a “risk-management” approach to monetary policy. In practice, risk management means considering all the significant risks (even the improbable ones) and setting policy to maximize benefits and minimize the costs. This means the Fed doesn’t automatically set its policy to the likeliest outcomes, but to the riskiest outcomes.

Right now, every member of the Fed policy committee judges that persistently high inflation carries the most risk. But that doesn’t mean there aren’t other risks to consider.

Breaking news: Fed’s Bullard says he is leaning toward backing 0.75 percentage point hike in September

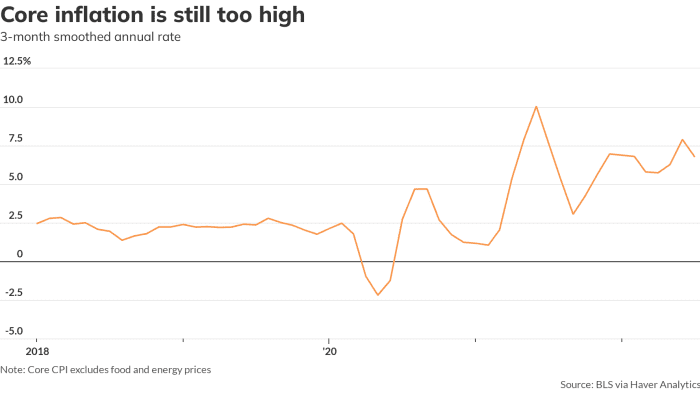

There is no hint that inflationary pressures are subsiding.

MarketWatch

Toothless Fed

The July 26-27 minutes mention two other significant risks. The first one is that the public won’t believe the Fed when it says its top priority is to kill inflation even if that means falling asset prices SPX, +0.23% DJIA, +0.06% and higher unemployment rates. If the public did come to believe that the Fed is toothless, it would start expecting much higher inflation in the future. And, according to theory, that would fuel even more inflation and make it even more difficult to get inflation bottled up in the 2% range.

The Fed’s fear is justified: The Fed has a reputation for cutting rates and printing money whenever the financial markets catch a little cold. Markets still believe in the Fed put, and the only thing that will persuade investors that the put is gone for good is for the Fed keep fighting the war against inflation regardless of bear market or recession.

This risk argues for a hawkish Fed.

Breaking news: Fed’s Kashkari says he doesn’t know if the central bank can bring inflation down without triggering a recession

The second risk cuts the other way. The minutes reported that “many” participants (which is taken to mean at least five but less than nine) mentioned the risk that the Fed might raise interest rates more than necessary to fight inflation. If that happened, the Fed would have smothered the economy needlessly, failed to achieve its goal of maximum employment, and put its political independence at risk.

This risk argues for a dovish Fed…eventually. No one at the Fed believes policy makers have already gone too far; that is something to worry about next year or the year after. But it was this comment that led to the markets misunderstanding the Fed’s commitment to wringing the inflation out of the economy.

Breaking news: Fed doesn’t want to ‘overdo’ rate hikes, San Francisco president Daly says

The Fed has to consider all the significant risks, but just talking about a risk doesn’t mean the Fed will act on it. I’d wouldn’t be surprised if everyone (not just “many”) on the Fed committee believes that hard landing (a job-killing recession) from overtightening is a real risk. After all, the Fed almost always goes too far, one way or the other.

High bar before reversing course

But there’s no hint in the minutes that the Fed is starting to get cold feet about raising rates quite a lot over the next 12 months or so. Accordingly, the fed funds futures market is pricing in only a slim chance of a rate cut in the first half of 2023. As recently as Aug. 4, the futures market was expecting the Fed to cut interest rates by a quarter-point by July 2023.

The overwhelming message from the Fed in recent weeks and months is that it will do what’s necessary to achieve price stability.

The bar is very high for the Fed to reverse course. It won’t happen while inflation is still burning red hot.

Don’t just take my word for it.

Listen to Andrew Hollinghorst, chief U.S. economist at Citi: “A committee that values its ‘resolve’ in fighting inflation is unlikely to turn substantially more dovish so long as underlying inflation remains well above target and is not convincingly slowing.”

Here’s Mark Haefele, chief investment officer at UBS Global Wealth Management: “In our view, three months in a row of subdued (core PCE of no more than

+0.2% month-over-month) price increases is the minimum requirement to

support a pause. We maintain our view that the Fed will raise rates by

another [percentage point] by year-end, with risks of more hikes if inflation does not slow in line with our forecasts.”

The Fed is not playing games. Of course Fed is trying to manipulate us, but it’s doing so in plain sight. The Fed is telling us clearly what it thinks and what it plans to do. It abandoned the mysticism of Alan Greenspan long ago, but for some reason many market participants and media mavens insist on parsing every word of Fed communications to discover the secret meaning.

There is no secret to the Fed’s battle plan. Such plans always change, of course, but only when the situation demands it. For now, the Fed’s plan is a direct frontal assault on inflation regardless of collateral damage.

It really means it.

Rex Nutting is a columnist for MarketWatch who’s been writing about the Fed and the economy for more than 25 years.

More by Rex Nutting

Inflation hasn’t peaked yet because rents are still rising fast

Wages are still rising faster than the Fed will tolerate. That means more rate hikes and layoffs are coming.

Everything you need to know about the economic recession that we are definitely not in right now