in New York, U.S., on Tuesday, Sept. 7, 2021. Equities retreated from near-record highs as U.S. trading resumed after the Labor Day holiday. Photographer: Michael Nagle/Bloomberg")

A trader works on the floor of the New York Stock Exchange (NYSE) in New York, U.S., on Tuesday, Sept. 7, 2021. Equities retreated from near-record highs as U.S. trading resumed after the Labor Day holiday. Photographer: Michael Nagle/Bloomberg

Four major events over the next 13 trading sessions will be the key catalysts in determining whether this year’s stock-market revival gets derailed or starts rolling again after a February slump.

It all begins Tuesday, when Federal Reserve Chair Jerome Powell delivers his two-day biannual monetary policy testimony on Capitol Hill. With the S&P 500 Index coming off its best week in a month, investors will be searching for any hint on the central bank’s interest-rate hiking path.

“The market is clinging to every single positive thing Powell says,” Emily Hill, founding partner at Bowersock Capital, said. “The minute the word ‘disinflation’ left his lips in a speech earlier this year, the market soared.”

Indeed, the rally at the end of last week was spurred by Atlanta Fed chief Raphael Bostic saying the central bank could pause this summer.

After Powell, comes the February jobs report on March 10 and consumer-price index on March 14. Another hot reading on employment growth and inflation could dash any hopes that the Fed will pullback soon.

“There are such conflicting signals in the economy,” Hill said. “So you’re going to see overreactions from investors to the upcoming data.”

Then, on March 22, the Fed will give its policy decision and quarterly interest-rate projections, and Powell will hold his press conference. After that, investors should have a pretty clear idea of whether the central bank will halt its rate hikes some time in the coming months.

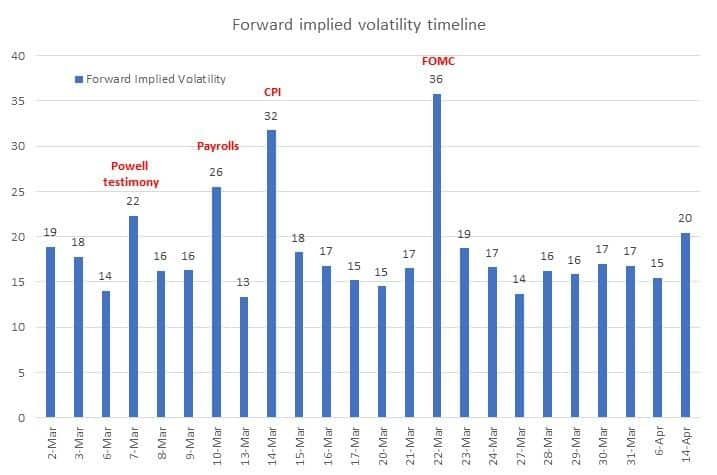

Investors are anxious about most of this. Forward implied volatility is back in the low 30s for the consumer-price-index day and nearing 40 for Fed rate-decision day later, meaning traders are betting on some big swings, data compiled by Citigroup show. However, a forward implied volatility reading of 26 on jobs data day indicates the market is underpricing that risk, according to Stuart Kaiser, Citigroup’s head of US equity trading strategy.

As for the stock market itself, the prevailing sense has been calm. The S&P 500 posted a daily move of less than 0.5% in either direction for the three-trading days ending March 1, a streak of tranquility last seen in January when investors boosted their bets that the US economy may avert a recession as inflation ebbs.

Source: Citigroup

Source: Citigroup

Here’s what traders will be monitoring.

Powell Testimony

The Fed chair’s biannual monetary policy report to the US Senate Banking Committee on Tuesday and the House Financial Services Committee on Wednesday are likely to offer hints on the US economic outlook, specifically inflation, wage pressures and employment. Traders will also look for clues on additional steps the Fed will take to control elevated prices.

Jobs Report

The labor market was strong in January. That’s an important driver of inflation, because wage growth can keep prices higher. And it’s a risk for stock prices because sticky inflation would prevent the Fed from pausing rate hikes. Economists predict that the February unemployment rate will come in at 3.4%, unchanged from January. Nonfarm payrolls growth is expected to drop to 215,000 after a surprising burst of 517,000 jobs a month earlier. But ultimately the data comes down to wages and whether the Fed thinks they’re slowing fast enough to drive inflation lower.

Inflation Data

The February consumer price index reading is crucial, after it jumped to start the year. Any sign of persistent inflation could push the Fed to raise rates even higher than already expected. The forecast for February’s CPI is 6%, an improvement from January’s 6.4%. Core CPI, which strips out the volatile food and energy components and is seen as a better underlying indicator than the headline measure, is projected to rise 5.4% from February 2022 and 0.4% from a month earlier. The Fed’s inflation target, which takes in more than just the CPI reading, is 2%.

Fed Decision

The market is pricing in a September peak in interest rates at 5.4%, nearly a percentage point above the current effective federal funds rate. Traders are preparing for the possibility of the Fed returning to jumbo rate hikes, with overnight index swaps pricing in about 31 basis points of tightening later this month.

Of course, the Fed’s forward expectations and Powell’s comments after the decision will affect market sentiment. But it’s about big misses, like inflation readings coming in much hotter than expected, that would derail the stock market’s recovery attempts, according to Michael Antonelli, market strategist at Baird.

“If the terminal rate goes from 5% to 5.5%, that will be a headwind, but it won’t crater the stock market the way it did last year,” Antonelli said in a phone interview. “Last year, we didn’t know what the worse-case scenarios was going to look like, but this year the window of potential outcomes is much narrower. And investors like that.”