“Low inflation is indeed the problem of this era.” Thus said John Williams, president of the Federal Reserve Bank of New York, in late 2019, espousing the dominant view at the time. Fast forward to the present, and the problem is the exact opposite. Just about every country in the world has grappled with soaring prices in 2022. The situation is all but certain to improve in the coming year, but at a severe cost to economic growth.

What made 2022 so unusual was the breadth of price pressures. The global rate of inflation will finish the year at roughly 9%. For many developing countries high inflation is a recurrent challenge. But the last time that inflation was so elevated in rich countries was the early 1980s. In America consumer prices are on track to have risen by about 7% in 2022, the highest in four decades. In Germany the rate will be closer to 10%, its first bout of double-digit inflation since 1951.

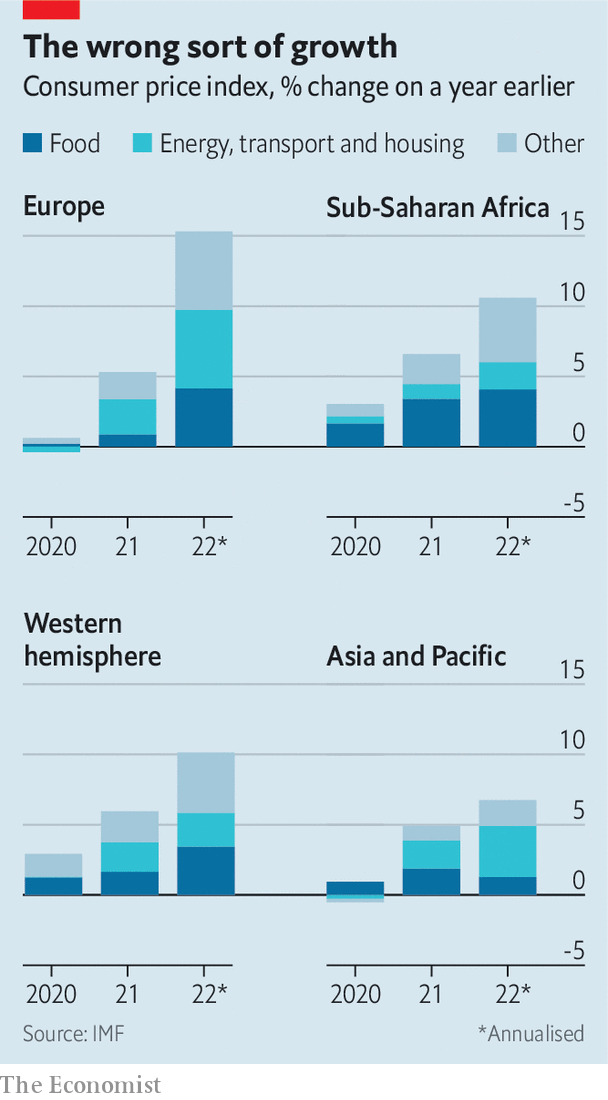

The common factors driving up inflation everywhere were soaring fuel and food costs. Prices for many consumer goods were already trending up at the start of 2022 because of covid-19’s lingering impact on supply chains. Russia’s invasion of Ukraine in February proved even more disruptive. The cost of oil climbed by a third as Western countries slapped sanctions on Russia, a major crude producer. Food prices also surged, pushed up by fertiliser and transportation costs as well as by Russia’s blockades of grain exports from Ukraine, a major wheat producer. In economic terms, this amounted to a classic supply shock. The sudden rise in prices for key commodities quickly filtered into daily life for the world’s citizens. In Europe, long reliant on Russian gas, millions will struggle to afford heating this winter. Across all regions, food and fuel accounted on average for more than half of inflation in 2022 (see chart).

Were inflation just a supply-side phenomenon, it would have been painful enough. But the most worrying development for central bankers was that pressures seeped into “core” components of price indices—that is, goods and services other than volatile food and energy. The rise in core prices was an indication that inflation was gathering momentum all of its own. That, in turn, pointed to causes beyond the oil shock. Many countries now have ultra-tight labour markets, partly a result of a wave of early retirements during covid. As a result companies are paying higher wages to attract workers, adding to inflationary momentum. In America, where the rise in core inflation was particularly steep, an additional culprit was excessive stimulus—by both the government and the Fed—at the height of covid. For much of 2022 that translated into overheated demand, with real personal spending higher than the pre-pandemic trend. Tellingly, the big economy with the lowest inflation was China. Its “zero-covid” strategy pushed spending far below the pre-pandemic trend.

Almost everywhere there was anxiety that rising prices would reset people’s inflation expectations, leading them to demand higher pay. Known as a wage-price spiral, such a dynamic would make inflation far harder to eradicate. The mere threat of the dynamic was sufficient to stir central banks to action. The Fed was the most aggressive, raising interest rates from a floor of zero in March to more than 4% today, its sharpest dose of monetary tightening in four decades. Central banks throughout the rich world, from Stockholm to Sydney, followed in its wake.

One way of looking at inflation prospects for 2023 is as a duel between rebounding supply and falling demand. Promisingly, some of the factors that fuelled inflation early in 2022 have started to fade. Prices of consumer goods have declined as supply chains have returned to normal. The cost of oil has fallen back to its level a year ago, in part thanks to a recovery in production. Tighter monetary policy works by choking off demand, and that is starting to happen, too. The most rate-sensitive sectors are suffering the most: a sudden chill has settled over once-sizzling property markets, with transactions drying up. If the recovery in supply—including, crucially, of willing workers—is big and fast enough, central banks may be able to stop tightening before provoking a deep recession. But at this point it seems more likely that they will exact a real toll on the global economy. In 2023 fears of inflation may give way to concerns about unemployment. ?