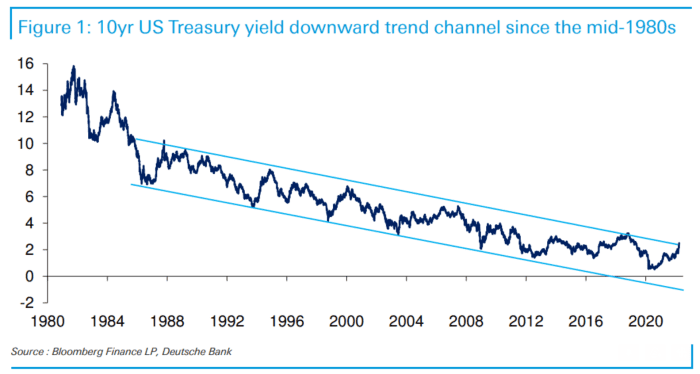

Yields on the 10-year Treasury note have spiked through the top line of a downward trend channel tracing back to the mid-1980s, with surging inflation and the Federal Reserve’s reaction to it sparking questions over whether the long-term trend will imminently end, according to a research note from Deutsche Bank.

“Clearly such a channel can’t go on forever unless you’re of the opinion that we will consistently see negative nominal US yields in the latter part of this decade,” Jim Reid, head of thematic research at Deutsche Bank, said in an emailed note Monday that illustrated the downward trend. “So the near 40-year trendline will almost certainly have to end in the next few years regardless, but the recent spike in yields raises the prospect of it doing so imminently.”

DEUTSCHE BANK RESEARCH NOTE

“The dam finally broke last week with yields rocketing up as markets woke up to the reality that every upcoming FOMC meeting could bring” a rate hike of 50 basis points, Reid wrote in a separate note, on macro strategy, Monday. “An array of Fed speakers during the week either endorsed this or didn’t rail against it too strongly.”

Last week the yield on the 10-year Treasury note surged 34.5 basis points to 2.491% on Friday, the largest weekly increase since September 2019, according to Dow Jones Market Data. That’s the highest yield since May 6, 2019 based on 3 pm Eastern Time levels.

At the conclusion of its Federal Open Market Committee meeting on March 16, the Federal Reserve raised its benchmark interest rate for the first time since 2018, in a step toward combating high inflation. The Fed hiked its rate 25 basis points from near zero, and has signaled a further tightening of its monetary policy this year.

Read: U.S. inflation rate climbs again to 7.9%, CPI shows, and Ukraine war threatens more pain for consumers

Meanwhile, “the fact that the last decade was so moribund from an activity and inflation point of view means that markets still refuse to believe the Fed can get very far in this cycle,” according to Reid.

If the post-Global Financial Crisis cycle “could be erased from people’s memory banks,” then markets might be pricing 300 to 400 basis points of hikes this year rather than around 240 basis points now priced in, Reid wrote in his note highlighting the chart. That’s “given just how far the Fed is behind the curve.”

“Overall there has been a constant misunderstanding of this cycle,” Reid said. “The market is collectively anchored to the trends of the last cycle.”

Before the FOMC meeting in June 2021, “the Fed and the market were hardly pricing in any rate moves until 2024,” he said, “and only 3 hikes for 2022 as recently as the start of this year.” The amount of rate hikes now priced in by the market for 2022 “still isn’t a huge year of tightening historically,” said Reid.

Despite the spike higher in 10-year Treasury yields, “real interest rates remain solidly negative,” according to a DataTrek Research note emailed Monday morning.

In 2013, a “tantrum” in the bond market “pushed real rates from similar levels to positive over the course of a month,” DataTrek co-founder Nicholas Colas said in the note. DataTrek co-founder Nicholas Colas said in the note. “The rapid shift in market sentiment related to the first one and now several 50-basis point rate hikes this year could be what causes the 2022 version of the 2013 Tantrum.”

The 10-year Treasury yield TMUBMUSD10Y, 2.400% was down about 2 basis points Monday afternoon, trading around 2.46%, FactSet data show, at last check.

The recent move higher in 10-year Treasury yields is probably not over, according to the DataTrek note. “Real rates can – and should – go positive,” Colas wrote. “Upcoming economic data will almost certainly show continued inflation pressures.”

The next reading on inflation, as measured by the personal consumption expenditures price index, is due out Thursday.

Meanwhile, the closely watched spread between 2-year and 10-year Treasury yields remains positive, “which is good news,” said Colas. An inversion of that portion of the yield curve, seen when the yield on the 2-year Treasury rises above the 10-year Treasury yield, has historically signaled a looming recession.

See: Treasury yield curve risks inverting relatively early after start of Fed rate hike cycle, warns Deutsche Bank

“With still-positive spreads, Treasuries are saying that the Fed is not going to ‘overtighten’” and cause a recession, according to Colas. “The 2/10-year spread captures the anticipated rate hikes in the back half of 2022 and into 2023.”

Ten-year yields minus 2-year yields came to 18 basis points on Friday, according to data from the Federal Reserve Bank of St. Louis. That compares with a spread of 30 basis points on March 15, the day before the Fed announced it was raising its benchmark rate from near zero.

On Tuesday afternoon, Bloomberg reported that the yield curve briefly inverted, with the U.S. 2-year yield exceeding the 10-year yield for the first time since 2019. While that brief inversion flashed a warning that the Fed’s rate hike cycle could tip the economy into a recession, the spread between 2-year and 10-year yields returned to a positive spread of about 5 basis points based on 3 pm Eastern Time levels Tuesday, according to Dow Jones Market Data.

The spread between 3-month and 10-year yields in the U.S. Treasurys market has been another reliable indicator of recession, but it’s “useless right now because we know the Federal Reserve plans a long series of rate hikes and these extend beyond a 3-month window,” Colas said.