hiked fuel prices across metropolitan cities on May 4.")

Oil marketing companies (OMCs) hiked fuel prices across metropolitan cities on May 4.

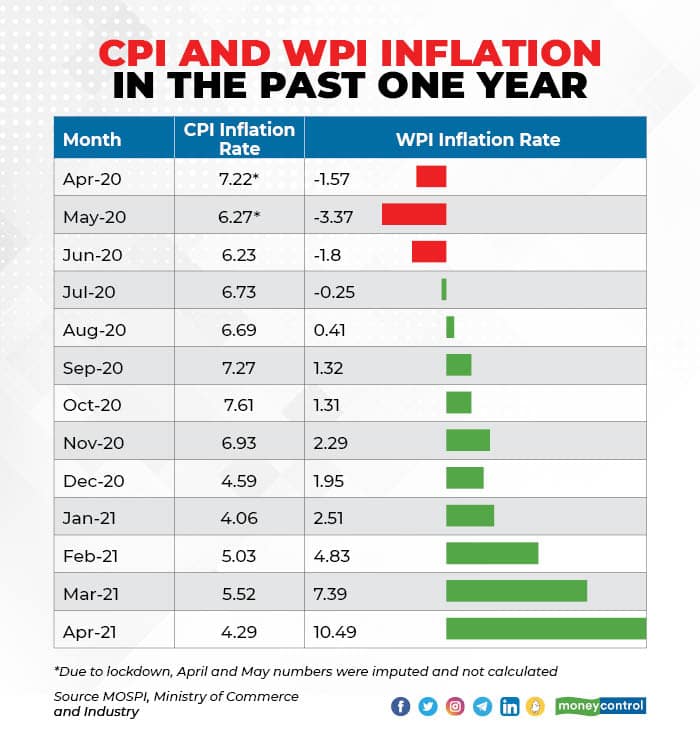

Wholesale price Index (WPI)-based inflation, which in April touched an 11-year high of 10.49 percent, is expected to remain high in the coming months due to a low-base effect and sustained high commodity prices. However, since overall growth in the Indian economy is also showing good numbers due to the same low-base effect from 2020-21, there is no fear of stagflation, economists told Moneycontrol.

Data on May 17 showed that WPI inflation had reached near record levels owing to rising fuel and power prices, that reached a 49-month high, and a rise in global commodity prices as other nations come out of the COVID-19 pandemic.

These factors cancelled out a fall in food prices across-the-board, as non-food WPI inflation rose a 15.6 percent compared with a 3 percent deflation for the same period last year.

“WPI will remain elevated in the months to come for two reasons: rising global commodity prices and low base effect. This may sound good for corporates who could be regaining some purchasing power,” said Madan Sabnavis, Chief Economist with Care Ratings.

Sabnavis said that WPI, or ‘factory gate’ inflation is expected to be close to double digits in the coming months, while consumer-price index-based inflation (CPI) or retail inflation will remain comfortably within the target range of the Monetary Policy Committee (MPC).

“We expect the headline WPI inflation to rise further to 13-13.5 percent in the current month before commencing a downtrend, whereas the core-WPI inflation may continue to rise over the next three prints to a peak of around 10.5 percent,” Nayar said.

“The advanced economies have been able to ramp up vaccinations due to smaller populations, compared to India. That optimism is fueling commodity prices when at a time our own sentiments have weakened,” Nayar said, adding that this could be a cause of concern.

Nayar said that April’s spike in WPI was led by an unexpectedly large surge in the inflation for manufactured products and food items, which was accompanied by an anticipated spike in minerals and fuels, led by the low base, rise in commodity prices and weakening rupee.

No stagflation worries

By definition, stagflation means persistent high inflation combined with high unemployment and stagnant demand and low growth in a country’s economy. Economists said that this situation is unlikely in spite of high WPI inflation, as CPI inflation is manageable and growth this year is expected to be much higher than 2020-21 even after a number of brokerages have cut their forecasts.

The likely trajectory of the WPI inflation supports our view that there is no space for rate cuts to support the faltering growth momentum, even as we expect the monetary stance to remain accommodative.

“It is too early to talk about stagflation. You will still end up with high growth as far as year-on-year comparisons are concerned,” Nayar said.

“Stagflation is out of the question technically because we are not getting negative growth. Though growth forecasts for the year have been reduced, they will still be much higher year-on-year. As for unemployment was increasing even before the pandemic,” Sabnavis said.

Another startling trend has been the wide divergence between CPI inflation and WPI inflation (see chart). The economists say that this is expected and should not be a concern for policymakers since the MPC’s focus is on retail inflation.

“When you have a surge or a collapse in commodity prices, there is a divergence between CPI and WPI numbers. CPI is driven by food prices and WPI is much more driven by commodity prices. This has happened in the past and can happen again. The prices of finished products and services don’t change so fast,” Nayar said.